Alistair Berg/DigitalVision through Getty Photos

When IT involves investing, understanding when to promote is equally essential to understanding what and when to purchase. I’ve had my justifiable share of circumstances the place I purchased one thing, shares shoot up, and earlier than I can promote IT, shares plummet to a worth beneath what they had been buying and selling at earlier than I bought them. That is one of many worst emotions on the planet. IT‘s mandatory for buyers to be taught from classes like that and to come back to know when IT is sensible to exit a chance. One agency, for example, that I’m now turning extra impartial on is Packaging Company of America (NYSE:PKG).

For these not conversant in the enterprise, IT‘s a significant participant within the packaging trade. The corporate produces about 4.53 million tons of containerboard, 60.5 billion sq. toes of corrugated product shipments, and 472,000 tons of uncoated free sheet paper from the 8 mills and 86 corrugated merchandise crops that IT has unfold throughout North America. For some time now, I’ve been bullish on this area, together with this specific participant. And issues have gone fairly properly. Since I final wrote concerning the agency in a bullish article printed in June of 2022, shares have seen upside of 40.3%. That is barely higher than the 39.5% rise seen by the S&P 500 over the identical window of time. Even higher is the comparability when after I wrote concerning the enterprise initially in April of 2022. In that article, I additionally rated the corporate a ‘purchase’ to replicate my perception that shares ought to see upside that will outperform the broader market. Since then, the inventory is up 32.2% in comparison with the 14.4% seen by the broader market.

Sadly, among the basic knowledge reported by the corporate is now coming in worse than IT did the yr prior. That is making shares costlier. On an absolute foundation, the inventory will not be precisely dear. Nevertheless, analysts predict the close to future to end in much more ache for the enterprise. Whereas IT is feasible that the corporate might flip issues round when IT studies monetary outcomes for the primary quarter of its 2024 fiscal yr after the market closes on April twenty second, I’d argue that, given its relative valuation and up to date decline in profitability, IT is sensible to downgrade the agency to a extra modest ‘maintain.’

The image is worsening

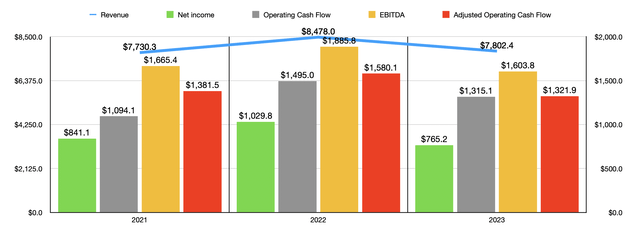

On this planet of packaging, Packaging Company of America is a large participant. Final yr, the corporate generated $7.80 billion in income. Whereas this does symbolize a rise over the $7.73 billion generated in 2021, IT really represents a significant decline from the $8.48 billion generated in 2022. The overwhelming majority of that drop got here from its Packaging phase, with income dropping 8.3% from $7.78 billion to $7.14 billion. Administration attributes this decline to decrease costs and product mixture of about $397 million and decrease volumes that hit income to the tune of $248 million. Throughout 2023, the corporate’s home containerboard costs dropped by 10.5%, whereas export costs plunged a outstanding 29.7%. Volumes shipped additionally fell, however this decline was extra modest. When IT got here to containerboard outdoors shipments, the decline was 1.1%. In the meantime, complete corrugated merchandise shipments dropped 4.6%.

Writer – SEC EDGAR Knowledge

Truthfully, I’m not stunned by this. For a few years in the course of the pandemic, packaging corporations had been capable of considerably hike their costs. They benefited tremendously from this, with earnings and money flows rising properly. However now, the shoe seems to be on the opposite foot. Sadly, that is having a detrimental influence on the corporate’s backside line as properly. Internet earnings has dropped from $1.03 billion in 2022 to $765.2 million final yr. Different profitability metrics adopted the same trajectory. Working money move went from just below $1.50 billion to $1.32 billion. If we alter for modifications in working capital, we get a decline from $1.58 billion to $1.32 billion. In the meantime, EBITDA additionally took a success, dropping from $1.89 billion to $1.60 billion. If these declines, relative to the drop in gross sales, seem steep, that is what occurs when worth declines account for a large portion of any drop in income.

Writer – SEC EDGAR Knowledge

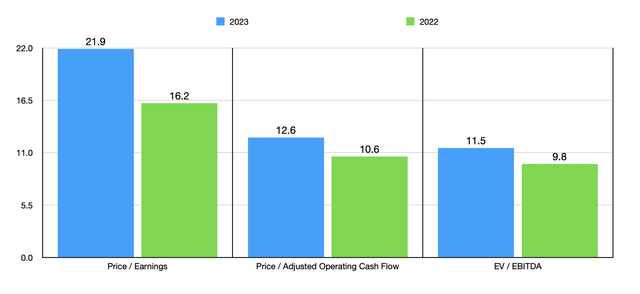

Even with this ache that the corporate has seen, shares do not look outrageously priced on an absolute foundation. Utilizing the info from 2023, I used to be capable of worth the corporate as proven within the chart above. For context, you can even see IT valued utilizing the info from 2022. On a worth to earnings foundation, shares have gotten costlier. The identical is true when IT involves each the worth to adjusted working money move foundation and the EV to EBITDA foundation. I’d name a worth to earnings a number of of 21.9 fairly lofty. However the different two profitability metrics look to be kind of within the truthful worth vary. However then, within the desk beneath, I made a decision to check Packaging Company of America to 5 comparable corporations. When IT got here to each the worth to earnings strategy and the worth to working money move strategy, IT ended up being the most costly of the group. And once we use the EV to EBITDA strategy, three of the businesses ended up cheaper, whereas one other was tied with IT.

| Firm | Value / Earnings | Value / Working Money Movement | EV / EBITDA |

| Packaging Company of America | 21.9 | 12.6 | 11.5 |

| Sonoco Merchandise Firm (SON) | 12.0 | 6.5 | 7.8 |

| WestRock Firm (WRK) | 9.5 | 6.9 | 64.3 |

| Graphic Packaging Holding Firm (GPK) | 12.3 | 7.8 | 7.8 |

| Sealed Air Corp. (SEE) | 14.1 | 9.4 | 9.6 |

| Amcor plc (AMCR) | 20.8 | 9.9 | 11.5 |

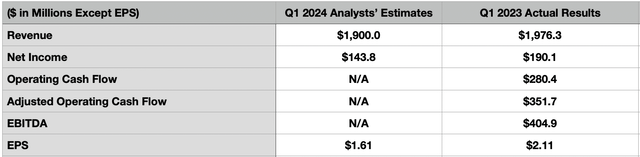

In fact, this image can change when earnings come out. And as I said already, the administration group on the enterprise is anticipated to announce monetary outcomes for the primary quarter of the 2024 fiscal yr after the market closes on April twenty second. Nevertheless, expectations do not seem like all that prime. Analysts are forecasting income, for example, of $1.90 billion. In the event that they grow to be appropriate, this can symbolize a 3.9% drop from the $1.98 billion generated the identical time of the 2023 fiscal yr.

Writer – SEC EDGAR Knowledge

On the underside line, there’s additionally the expectation of continued weak point. Earnings per share are forecasted to be $1.61. That is down from the $2.11 that the corporate reported within the first quarter of 2023. If this seems to be appropriate, IT would translate to web earnings falling from $190.1 million to $143.8 million. Sadly, we do not have estimates when IT involves different profitability metrics. However within the desk above, you possibly can see working money move, adjusted working money move, and EBITDA for the primary quarter of 2023. In all probability, if analysts are appropriate, these can even be decrease this yr.

IT needs to be said that analysts aren’t the one ones with dour expectations. Administration did say that complete corrugated product shipments, pushed by robust demand and two extra working days, ought to result in ends in the primary quarter of 2024 being stronger than what they had been within the ultimate quarter of 2023. Nevertheless, they anticipate containerboard quantity dropping due to a chronic outage at considered one of its mills and a scheduled upkeep outage at one other. Costs and product combine must also assist to some extent, for the reason that firm did provoke new worth will increase in January. However even with that, they anticipate containerboard costs to be flat. There are another weaknesses, reminiscent of when IT involves wages due to seasonal timing associated will increase. However past saying that earnings within the first quarter might be decrease than what they had been within the ultimate quarter of final yr, administration has not supplied a lot in the best way of steerage.

Takeaway

Based mostly on the info supplied, I imagine that now’s the time to think about trying elsewhere for alternatives. The trip larger for Packaging Company of America and its buyers has been nice. The inventory has outperformed the broader market, even at a time when fundamentals have weakened. In some unspecified time in the future, IT would possibly make sense to step again in. However that may solely be if shares fall from right here or if fundamentals decide up. As a consequence of these ideas on the matter, I’ve determined to downgrade the inventory from a ‘purchase’ to a ‘maintain’.