jetcityimage

Lucid Group (NASDAQ:LCID) acquired a brand new $1.5B lifeline from Saudi Arabia’s Public Funding Fund that’s set to assist the electrical automobile firm help the manufacturing ramp of its latest electrical automobile mannequin, the Gravity SUV. The corporate additionally delivered blended outcomes for its second fiscal quarter final week, and Lucid maintained its manufacturing steerage of 9k EVs for FY 2024. Lucid did see an upswing in deliveries within the second quarter, however the EV maker stays broadly unprofitable and faces a difficult uphill climb going ahead!

Earlier ranking

I rated shares of Lucid a robust promote in my prior work on the EV maker — The Subsequent Fisker? — as the electrical automobile firm confronted a weak demand outlook, slowing prime line development and an unfavorable earnings image. Nevertheless, Lucid tends to haven’t any subject elevating capital from its wealthy Saudi Arabian backer, the Public Funding Fund, which simply dedicated one other $1.5B to the struggling electrical automobile maker. Since supply development got here in additionally stronger than anticipated, I’m altering my ranking to carry.

Stronger than anticipated supply ramp

Two of my key causes for down-grading shares of Lucid to robust promote in April have been Lucid’s underwhelming supply ramp, in addition to weakening demand for electrical automobiles extra typically. Nevertheless, deliveries within the second fiscal-quarter picked up for Lucid and the electrical automobile firm delivered 2,394 electrical automobiles, displaying a year-over-year development price of 70%. On the identical time, nonetheless, Lucid’s manufacturing totaled solely 2,110 electrical automobiles, displaying a 3% decline year-over-year.

Lucid

Importantly, Lucid didn’t elevate its electrical automobile manufacturing goal for FY 2024, indicating that the EV maker continues to see an total weak demand image. Lucid expects to supply 9,000 EVs this yr, implying a really average 7% year-over-year manufacturing development price.

Lucid, nonetheless, has one aggressive benefit over different electrical automobile corporations which is that Saudi Arabia’s sovereign wealth fund, the Public Funding Fund, is an anchor investor. Simply earlier than Q2’24 earnings, Lucid stated that the Public Funding Fund agreed to invest one other $1.5B within the type of most popular inventory and loans into the electrical automobile firm as a way to assist Finance the manufacturing ramp of the Lucid Gravity SUV, Lucid’s second main EV mannequin.

The Gravity SUV is about to see the beginning of manufacturing on the finish of the present fiscal yr. The $1.5B in money are a lot wanted as the corporate continues to lose a ton of cash even on its present manufacturing that features solely the Lucid Air and its varied higher-spec fashions. On the finish of the June quarter, Lucid had $3.9B in money sitting on its steadiness sheet, displaying a decline of $417M because the finish of FY 2023.

Lucid

What I dislike about Lucid, basically talking, is the very unfavorable earnings and free money circulation image. The EV maker misplaced a strong $643M within the June quarter, and its free money circulation is very destructive as nicely. Within the close to future, buyers will seemingly see an extra decline in free money circulation as the corporate ramps up its spending as a way to put together its manufacturing strains for the manufacturing of the Gravity SUV.

Lucid

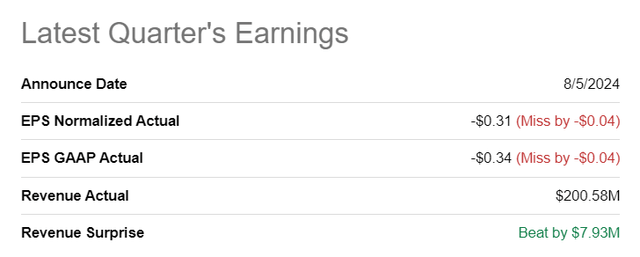

The weak profitability image was additionally the rationale why Lucid missed earnings expectations for the second-quarter. Lucid misplaced $0.31 per-share in Q2’24, lacking estimates by $0.04 per-share. Based mostly off of consensus estimates, the EV maker isn’t anticipated to be worthwhile till the start of the subsequent decade.

Searching for Alpha

Lucid’s valuation

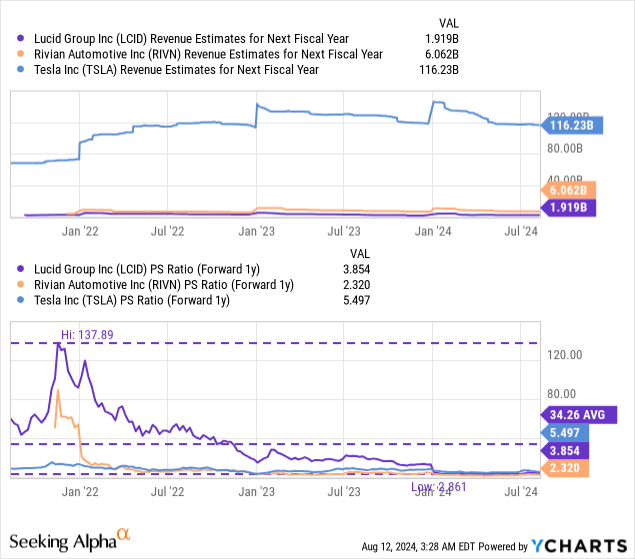

Lucid’s valuation continues to be stretched, for my part, particularly contemplating that the electrical automobile firm repeatedly in the reduction of on its supply targets up to now and isn’t but anyplace close to profitability on its present manufacturing line. Lucid is at present valued at a price-to-revenue ratio of three.8X and is due to this fact significantly dearer than Rivian Automotive (RIVN)… which I contemplate to be a lot better worth for EV buyers, particularly due to the corporate’s bettering unit economics and far greater manufacturing quantity. Rivian additionally lately struck a cope with Volkswagen to develop EVs collectively, which is bettering the danger profile for the U.S. firm. Tesla (TSLA), the market chief, is buying and selling at a P/S ratio of 5.5X.

I’d not need to pay greater than 3.0X income for Lucid, given its total low manufacturing quantity and chronic losses, nonetheless, and I see appreciable dangers on the horizon with the escalation of working losses as soon as the corporate ramps Gravity SUV manufacturing. This income multiplier would give the EV maker a good worth of $2.50 per-share.

Dangers with Lucid

The most important threat that I see for the electrical automobile maker is that the corporate will proceed to burn by means of a number of money and fail to considerably enhance its manufacturing output going ahead. Weak demand is clearly nonetheless a problem for the EV firm, in any other case Lucid would have raised its full-year manufacturing goal. What would change my thoughts concerning the electrical automobile firm is that if IT pulled off, in opposition to my expectations, a robust manufacturing ramp in FY 2025, pushed by the Gravity SUV and if Lucid’s profitability and free money circulation image drastically improved.

Remaining ideas

Whereas Lucid has seen a little bit of supply momentum in Q2’24 (which was a optimistic), the electrical automobile firm didn’t elevate its supply goal for the present fiscal yr. Lucid continues to challenge to supply 9k electrical automobiles this yr, and I don’t count on the corporate to see a elementary enchancment in its profitability or free money circulation image. The $1.5B funding of Saudi Arabia as soon as once more is essential to help the corporate’s Gravity SUV ramp, however in the end, buyers would need to see income and I stay extremely uncertain that buyers need to proceed to fund the agency’s working losses till the top of the last decade. With EV demand typically waning and Lucid reporting giant losses nonetheless, I don’t see a transparent path for an bettering profitability profile. I acknowledge, nonetheless, that PIF got here to the rescue of Lucid, which I why I’m up-grading shares to carry.

👇Observe extra 👇

👉 bdphone.com

👉 ultraactivation.com

👉 trainingreferral.com

👉 shaplafood.com

👉 bangladeshi.help

👉 www.forexdhaka.com

👉 uncommunication.com

👉 ultra-sim.com

👉 forexdhaka.com

👉 ultrafxfund.com

👉 ultractivation.com

👉 bdphoneonline.com

👉 Subscribe us on Youtube