Key Factors

- Tesla struggled in Q1 and is not anticipating enchancment till IT launches new merchandise subsequent yr.

- The long-awaited Mannequin 2 is again within the image and should come as quickly as early 2025. Fingers crossed.

- Analysts’ reactions are blended, however the internet result’s a downward motion within the consensus worth goal for this Maintain-rated inventory.

- 5 shares we like higher than Tesla

Tesla NASDAQ: TSLA shares are up greater than 10% following the Q1 earnings launch, and so they might transfer increased, however buyers shouldn’t anticipate a sustained rally; they need to solely anticipate volatility. The information driving the market is nice however so futuristic that IT is not going to affect operations positively for at the least twelve months. IT is nothing greater than a reduction rally.

Among the many drivers, no pun meant, are plans to construct out a robotaxi fleet, the lean into AI, and cheaper fashions. Between then and now, the corporate faces many headwinds, together with a tepid EV market, fierce competitors, tightening margins, and detrimental money circulate.

The analysts’ response aligns with the outlook for volatility. Analysts’ exercise is sizzling and blended, however the takeaway is a headwind for share costs. Extra analysts are decreasing their worth targets than elevating them, and a couple of improve is required to change the consensus score of Maintain, verging on Cut back. The consensus goal implies a 30% upside from the pre-release worth motion however is coming down rapidly and a cap to any rally that will type. The takeaway is that Tesla continues to be a dealer’s inventory and more likely to make some wild swings inside its buying and selling vary over the subsequent few quarters.

Tesla Had a Powerful Time in Q1

Tesla is in no hazard of implosion, however the Q1 outcomes and outlook for the yr counsel that the corporate’s struggles have but to finish. Q1 income fell 8.5%, the sharpest decline in over a decade, to $21.31 billion as a result of tepid demand development, weak deliveries, and the affect of worth and blend. The corporate issued quite a few worth cuts in most markets over the previous twelve months, impacting the highest and backside traces. The corporate has issued new worth reductions for the reason that finish of Q1, so they may proceed to affect because the yr progresses.

The affect of decrease costs was felt worse on the underside line. The corporate’s gross revenue fell by 18% on a 200 bps contraction in margin compounded by increased prices. Working margin fell by 592 foundation factors—revenue by 56% and adjusted earnings by 47%. The highest and backside traces have been worse than forecast, with income 415 foundation factors wanting the consensus reported by Marketbeat.com and earnings quick by 1000.

The steering is optimistic, however the optimism is offset by the continued expectation for weak spot this yr. Within the firm’s phrases, “In 2024, our car quantity development price could also be notably decrease than the expansion price achieved in 2023, as our groups work on the launch of the subsequent technology car and different merchandise.” Let’s hope these merchandise come to market in an affordable timeframe with out sudden prices. Tesla is greater than a automotive firm; an ecosystem is gaining leverage, however IT takes vehicles to make IT work.

Prices are additionally an issue. The corporate is leaning laborious into its subsequent development part, which is dependent upon AI, autonomy, and the long-anticipated Mannequin 2. FCF in Q1 got here in at a long-term low of -$2.53 billion, leading to a money draw on the steadiness sheet. The corporate is well-capitalized however goes to burn money this yr.

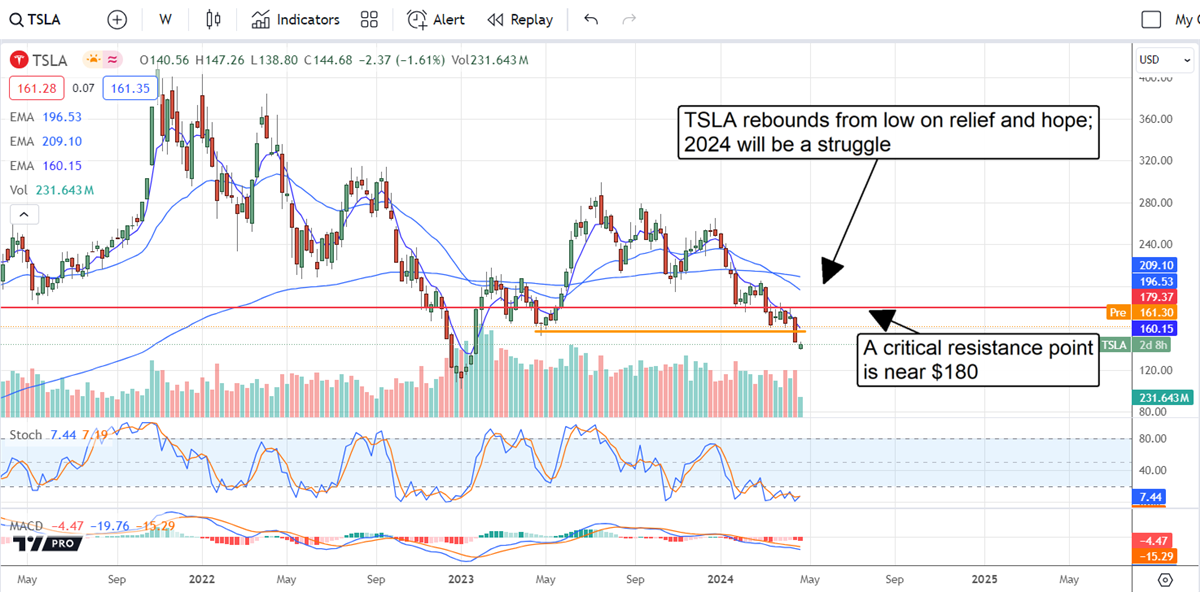

Tesla Rebounds: Important Resistance Lies Forward

The worth motion in Tesla has rebounded solidly following the report and should proceed increased. The caveat is that this market continues to be beneath a vital resistance level that would cap positive factors. That time is close to $180, and lows set in 2021. The $180 degree has been a set off level for consumers since then, and possibly once more.

Nonetheless, if this market can not get above $180 and maintain IT, the chances of a brand new low will develop. In that state of affairs, shares of Tesla will affirm resistance at a vital degree and will fall so far as $115 earlier than hitting stable assist. Even when the marketplace for TSLA can rise above $180, IT is not going to be out of the weeds. The long-term 150-day EMA and longer-term 150-week EMA are simply above and might also present important resistance to increased worth motion.

Earlier than you think about Tesla, you will need to hear this.

MarketBeat retains observe of Wall Avenue’s top-rated and finest performing analysis analysts and the shares they suggest to their purchasers every day. MarketBeat has recognized the 5 shares that prime analysts are quietly whispering to their purchasers to purchase now earlier than the broader market catches on… and Tesla wasn’t on the listing.

Whereas Tesla at present has a “Maintain” score amongst analysts, top-rated analysts consider these 5 shares are higher buys.

View The 5 Shares Right here

Click on the hyperlink beneath and we’ll ship you MarketBeat’s information to pot inventory investing and which pot corporations present probably the most promise.