Funtap Finance Technology Idea” data-id=”1304526076″ data-type=”getty-image” width=”1536px” peak=”681px” srcset=”https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w1536 1536w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w1280 1280w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w1080 1080w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w750 750w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w640 640w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w480 480w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w320 320w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w240 240w” sizes=”(max-width: 768px) calc(100vw – 36px), (max-width: 1024px) calc(100vw – 132px), (max-width: 1200px) calc(66.6vw – 72px), 600px” fetchpriority=”excessive”/>

Finance Technology Idea” data-id=”1304526076″ data-type=”getty-image” width=”1536px” peak=”681px” srcset=”https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w1536 1536w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w1280 1280w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w1080 1080w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w750 750w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w640 640w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w480 480w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w320 320w, https://static.seekingalpha.com/cdn/s3/uploads/getty_images/1304526076/image_1304526076.jpg?io=getty-c-w240 240w” sizes=”(max-width: 768px) calc(100vw – 36px), (max-width: 1024px) calc(100vw – 132px), (max-width: 1200px) calc(66.6vw – 72px), 600px” fetchpriority=”excessive”/>

Funding thesis

Digital outsourcing firm Conduent Integrated (NASDAQ:CNDT) is in the midst of a transition, one which IT hopes will return IT to profitability and progress. One essential factor of that transition includes promoting off a few of its subsidiaries and utilizing the money to scale back debt and make the agency extra nimble (its phrase).

Divestitures are continuing, and the corporate is making sluggish however regular progress towards its aim. Since Conduent generates income of greater than $3 billion a 12 months, a worthwhile earnings assertion might ship wonderful outcomes to shareholders.

Primarily based on that potential, I charge IT a Purchase, however traders will should be affected person.

About Conduent

In its 10-K for 2023, the corporate reported that IT supplies digital enterprise options and providers for the industrial, authorities, and transportation markets.

The agency provided examples of its tasks in its annual report: buyer expertise administration options for Virgin Atlantic, offering next-generation smartcard options for the State of Victoria in Australia, growing a brand new Medical Administration Information System for the State of New Mexico, and partnering with Schwab Retirement Plan Providers to broaden the capabilities of IT profit plans or shoppers.

Its strategic focus, in accordance with the 10-Okay, is:

“Our goal is to be the Technology-led enterprise options accomplice of selection for companies and governments globally. By means of our devoted associates, we ship mission-critical providers and options on behalf of companies and governments, creating precious outcomes for our shoppers and the hundreds of thousands of people that depend on them. To realize this, we concentrate on delivering outcomes throughout three essential dimensions: Development, Effectivity and High quality. Our technique is designed to ship shareholder worth by creating worthwhile progress, increasing working margins, figuring out course of efficiencies, and using a disciplined capital allocation technique.”

A part of its enchancment efforts contain divestitures, which CEO Cliff Skelton mentioned within the annual report, would streamline its portfolio and make IT a nimbler firm. Two gross sales have been accomplished in 2023 and on Could 3, 2024, IT introduced the sale of its Casualty Claims Options to MedRisk, a managed care firm. Apart from gathering $240 million from MedRisk, IT additionally helps Conduent concentrate on its core capabilities.

On June 10, IT introduced IT would spend about $132 million to repurchase shares from Carl Icahn and his associates. In a press launch, CEO Skelton mentioned, “Our choice to repurchase shares displays the boldness we’ve got in our enterprise, our technique and our long-term progress prospects”.

Conduent employed about 59,000 associates on the finish of 2023; 41% of them have been in North America and the remainder have been in Asia Pacific, Latin America, the Caribbean, and Europe.

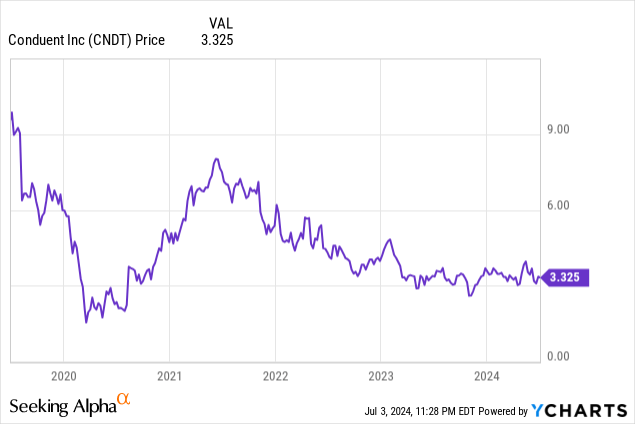

On the shut on July 3, IT was buying and selling at $3.33 and had a market cap of $691.49 million.

Monetary outcomes

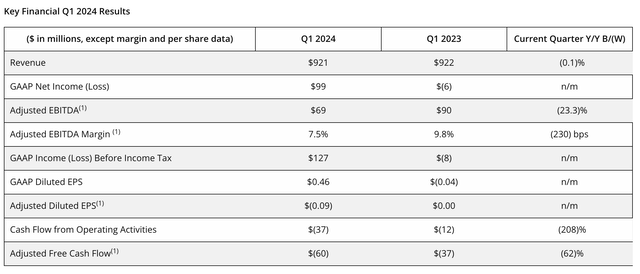

The corporate filed its first-quarter 2024 earnings report on Could 1st. The next desk from the report summarizes the outcomes:

CNDT Q1-2024 monetary outcomes (firm information launch)

Conduent attributed the flat income end result to the timing of “a number of alternatives” between the primary and second quarters of this 12 months.

Pretax earnings elevated from a lack of $8 million in Q1 of final 12 months, to a revenue of $127 million this 12 months, due to a $164 million achieve on the primary tranche from the BenefitWallet sale. The second tranches will present in Q2 earnings.

Utilizing proceeds from the primary and second tranches, IT pay as you go $259 million of principal on its Time period Loan B. Its steadiness sheet exhibits complete liabilities of $2.211 billion, together with $1.060 billion in long-term debt. On the opposite aspect of the ledger, IT confirmed complete property of $3.058 billion, together with $415.0 million in money and money equivalents.

Competitors for Conduent

The agency cites competitors in all of its classes; giant, multinational rivals embody Accenture plc (ACN), Cognizant Technology Options Company (CTSH), TTEC Holdings, Inc. (TTEC), and Teleperformance SE (OTCPK:TLPFF).

IT added that opponents vary from giants like these to comparatively small companies, however none competes throughout all the identical segments.

Conduent considers its onshore, close to shore, and offshore supply capabilities to be a aggressive benefit. Additionally within the 10-Okay, IT reported having a big portfolio of 631 patents and 7 pending functions, however that no single patent is important to its enterprise.

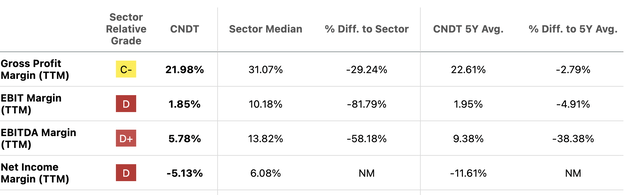

Its margins point out a slim moat, as proven on this excerpt from its profitability web page on In search of Alpha:

CNDT margins desk (SeekingAlpha )

Administration and technique

CEO, President, and director Cliff Skelton says in his company biography that he has “important expertise is large-scale operations and enterprise transformations, in addition to deep data of Technology.” Earlier than becoming a member of Conduent, he held senior management positions at Fiserv Inc. (FI), Ally Monetary Inc. (ALLY), and Financial institution of America Company (BAC). He beforehand served 20 years as a naval officer and fighter pilot.

Chief Monetary Officer Steve Wooden is claimed to have a “confirmed Finance government with a monitor file of driving worth in enterprise transformation and acquisition integration packages”. He, too, is an alumnus of Fiserv and is a Chartered World Administration Accountant with an MBA.

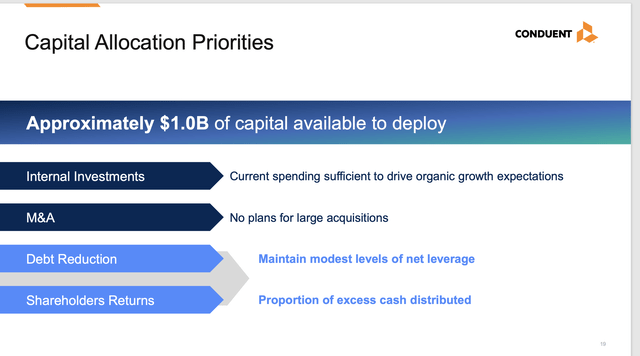

Luckily, each officers have transformation expertise, since that’s what they’ve undertaken with their efforts to streamline the portfolio and make Conduent nimbler. These targets, as articulated in its May 2024 investor presentation, inform its capital allocation technique:

CNDT capital allocation technique (investor presentation)

Development

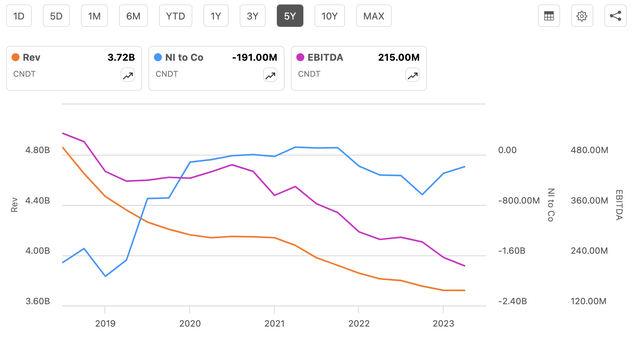

The necessity for a change is on show on this five-year chart of income, EBITDA, and web earnings:

CNDT income EBITDA NI chart (SeekingAlpha)

Declines in income and EBITDA predate the sale of its subsidiaries; by the divestments, Conduent takes in money and different property by the gross sales, however loses income and EBITDA that the divested companies would have supplied.

Don’t anticipate any dramatic enhancements this 12 months. In response to its outlook within the Q1-2024 reporting, IT expects income to drop from $3.722 billion in 2023 to $3.6000 billion – $3.700 billion this 12 months. For 2025, IT is projecting income of $3.000 billion to $3.300 billion.

The adjusted EBITDA margin is anticipated to shrink from 10.2% final 12 months to eight% – 9% this 12 months. On the optimistic aspect, adjusted free money stream as a share of adjusted EBITDA is projected to enhance, from minus 1.3% final 12 months to five% – 10% this 12 months.

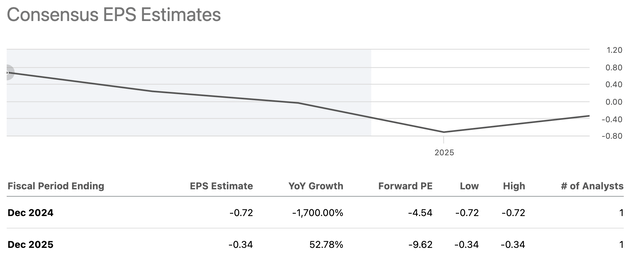

The 2 Wall Road analysts who comply with Conduent challenge related declines in income over this 12 months and subsequent. Additionally they see EPS bettering considerably in 2025:

CNDT EPS estimates (SeekingAlpha )

Feedback: anticipate little prime or bottom-line progress earlier than the tip of 2025. The corporate’s prime line is shedding income that has been introduced in by divested operations prior to now. The divestments are bettering the steadiness sheet on the expense of the earnings assertion.

Ultimately, Conduent’s streamlined portfolio ought to make the corporate worthwhile, extra resilient, and nimbler. For now, although, that future is at the very least a 12 months and a half away.

Valuation

With unfavorable earnings, traders should not have a few key valuation metrics: P/E and PEG. Nonetheless, these which might be obtainable are robust sufficient to present Conduent an total valuation grade of A-minus:

- EV/EBITDA [TTM]: 8.02 versus 12.64 for the Industrials sector median.

- EV/EBITDA [FWD]: 11.27 versus 10.99

- Value/Gross sales [TTM]: 0.19 versus 1.45

- Value/Gross sales [FWD]: 0.20 versus 1.41

- Value/Ebook [TTM]: 0.96 versus 2.69

- Value/Ebook [FWD]: 0.61 versus 2.60

- Value/Money Move [TTM]: 10.45 versus 13.54.

Conduent is undervalued by most measures, maybe as a result of traders have low expectations:

Having decided that IT is undervalued, the place ought to we anticipate the value to go within the subsequent 12 months, to the tip of the second quarter of 2025?

Because the chart suggests, traders have been in a holding sample for the previous 5 years, ready for at the very least a number of consecutive quarters of optimistic and growing profitability.

The 2 Wall Road analysts following Conduent have Sturdy Purchase scores and a median value goal of $5.71, together with a low of $4.14 and a excessive estimate of $7.00.

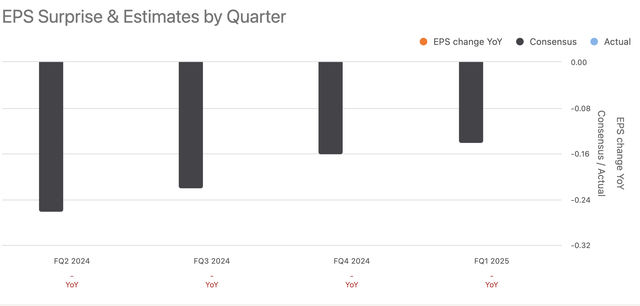

I’m much less optimistic than these analysts due to persevering with declines in income and the sluggish path towards profitability:

CNDT quarterly EPS estimates (SeekingAlpha)

My one-year goal value is the low estimate of $4.14, which remains to be a big achieve of 24.32%. I consider plenty of traders might monitor the inventory, hoping that its $3 billion plus income will finally yield critical web earnings and free money stream. If that does occur, and I anticipate IT will, the agency will be capable to spend money on new progress or present shareholders with buybacks or a dividend.

On that foundation, I charge Conduent inventory a Purchase. No different In search of Alpha analysts have posted a ranking prior to now 90 days, whereas the Quant ranking is a Maintain, and the Wall Road analysts posted two Sturdy Buys.

Threat components for Conduent

IT might by no means attain profitability, due to declining income and/or increased prices. IT operates in extremely aggressive markets, IT might run into issues with its divestments, and extra.

The share value trajectory has been down for the previous 10 years. In 2014, its share value was within the mid-teens, and rose to the low $20s again in mid-2018; since then, IT has been largely flat or down. Present shareholders might not keep, and potential traders won’t purchase due to low expectations.

Conduent seems to have solely a slim moat, that means IT won’t have as a lot pricing flexibility as IT must land new contracts or renew current contracts at worthwhile charges. That’s offset to some extent by its growing partnerships with different giant corporations.

As IT explains within the 10-Okay, IT typically makes “important” capital and different investments upfront in its contracts. That features the acquisition of Information Technology gear, facility prices, labor, and different prices which may not be recouped if the consumer fails or workout routines its termination rights.

A lot of its income comes from outsourcing, and if the pattern towards outsourcing reverses, its enterprise might be materially broken. Some companies can and do transfer providers again in home after transferring in the other way.

Conclusion

I contemplate Conduent to be an organization with promise, one that would reward shareholders. However that’s provided that IT retains pushing ahead and turns itself right into a revenue maker quite than a revenue loser.

If IT continues to make progress within the subsequent 12 months, even when IT doesn’t absolutely attain profitability, I consider the share value might improve by as much as 1 / 4, particularly by 24.32%. That gives the underpinning for my Purchase ranking

👇Comply with extra 👇

👉 bdphone.com

👉 ultraactivation.com

👉 trainingreferral.com

👉 shaplafood.com

👉 bangladeshi.help

👉 www.forexdhaka.com

👉 uncommunication.com

👉 ultra-sim.com

👉 forexdhaka.com

👉 ultrafxfund.com

👉 ultractivation.com

👉 bdphoneonline.com

👉 Subscribe us on Youtube