Andre Schoenherr

Introduction

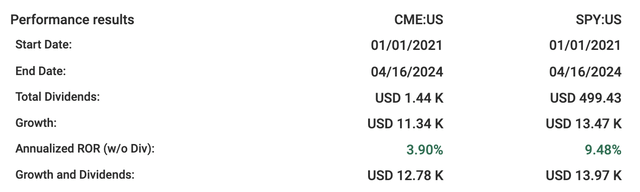

CME Group (NASDAQ:CME) is actually not a market-darling proper now. In a interval when SPY returned 9.48%, CME managed a measly 3.90%. An funding in SPY even yields extra dividends than the same one in CME. Ought to buyers take into account CME?

Fastgraph

On this article, I shall look at the bull and bear thesis for CME, and let’s begin with the dangers of investing within the firm.

Dangers: 3 Causes to Keep away from CME

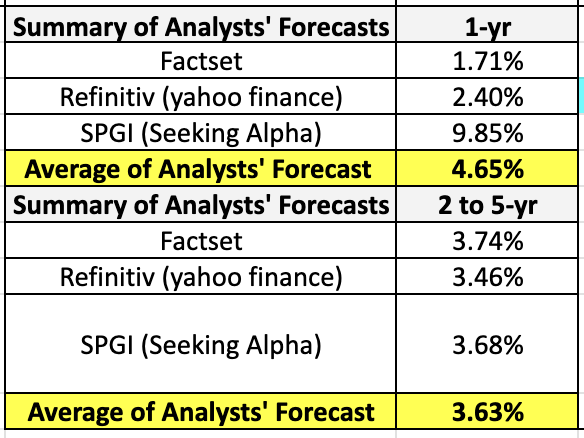

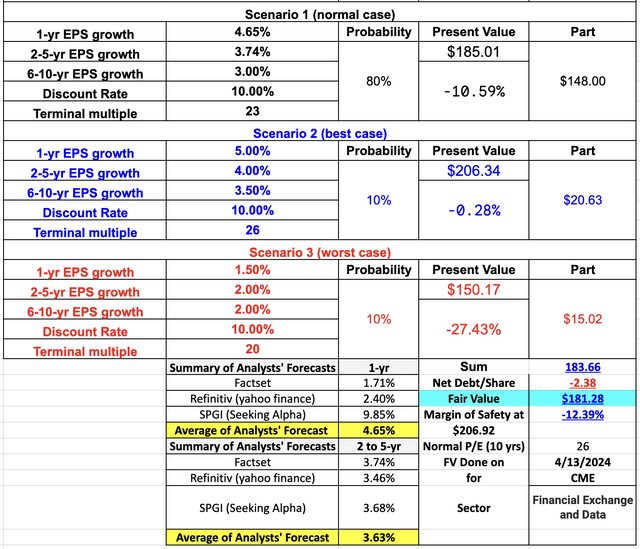

Firstly, this enterprise just isn’t anticipated to develop a lot within the quick time period. Analysts will not be anticipating the corporate to develop income a lot in 2024. The common 1-year earnings development forecast is within the mid-digit vary of 4.65%. The two-to-5-year earnings development forecast is even decrease at 3.63%.

Analysts’ compilation of analysts’ earnings development forecast

The steerage given by CFO Lynne Fitzpatrick at the This fall 2023 convention name concurred with analysts’ estimates:

Assuming comparable buying and selling patterns as 2023, the payment changes would improve futures and choices transaction income roughly 1.5% to 2%. Taken in combination with the payment adjustments for market information and non-cash collateral which took impact January 1st, the payment changes would improve complete income by roughly 2.5% to three% on comparable exercise to 2023.

Secondly, good cash is giving CME the snub regardless of its excellent efficiency in 2023.

The corporate did rather well from 2022 to 2023, boosting income by 11% from to $5.6 billion, and in This fall 2023 itself, CME generated greater than $1.4 billion in income, a 19% improve from This fall 2022.

Fintel

But, over the previous 6 months, analysts from Goldman Sachs, Rosenblatt, and Deutsche Financial institution downgraded the CME Group.

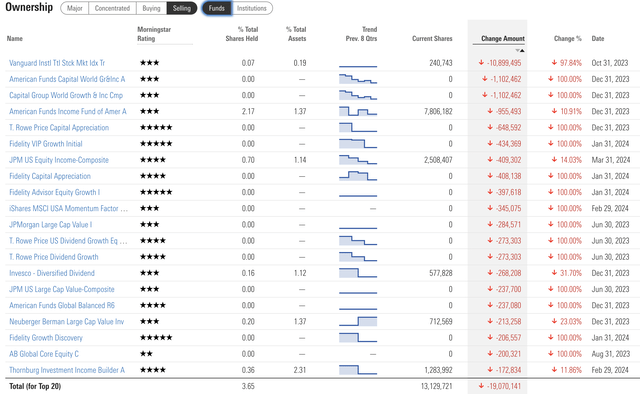

Furthermore, funds have been promoting their CME shares. Most of them offloaded 100% of their stakes within the firm.

Morningstar

And surprisingly, there aren’t any establishments and funds shopping for CME shares.

Morningstar Possession

The next remark from Morningstar’s analyst Michael Miller might clarify the rationale behind adverse sentiment that good cash presently has,

CME Group has loved favorable market situations in 2022 and 2023 as volatility throughout a number of asset lessons drove elevated buying and selling quantity, resulting in robust income development. Previous to 2022, probably the most important headwind for the corporate had been the impression that low short-term rates of interest had on its rate of interest futures, that are its largest income. When rates of interest are anticipated to remain low there may be much less want for rate of interest hedging and fewer incentive for hypothesis, making a drag on CME’s buying and selling quantity. With rates of interest now properly above the 0% charge we noticed throughout a lot of the previous decade, the drag has been eliminated, benefiting the corporate’s development. That stated, this was a one-time profit, and we anticipate CME’s income development to return to the low to mid single digits going ahead, notably as 2023 featured unusually giant value will increase from CME.

Retail buyers don’t transfer the market; IT is the massive boys. And if institutional buyers are avoiding CME, IT may very well be a protracted look ahead to its worth to be recognised.

Thirdly, as a worth investor, CME doesn’t appear to be buying and selling at any vast margin of security. Primarily based on my discounted money circulation mannequin, CME trades at 13.47% above my intrinsic worth.

Fastgraph

Once I ran a dividend low cost mannequin to estimate its honest worth, I arrived at only a barely increased honest worth of $192.05 which remains to be beneath its present market value. Comparatively, Morningstar assigned the next honest worth $225.

Nevertheless, there are features of CME Group that attracted me to present IT a re-examination.

Rewards: 6 Causes Why CME Group Is A Robust Enterprise

Let’s begin by addressing the danger that’s scaring institutional buyers away, that the Finance.yahoo.com/information/fed-dot-plot-suggests-central-bank-will-cut-interest-rates-3-times-in-2024-180543905.html?fr=sycsrp_catchall” rel=”noopener”>Feds may very well be slicing rates of interest in 2024 by as many as thrice.

Firstly, the unsure rate of interest surroundings will be the factor that creates alternatives for worth buyers. CME CEO Terry Duffy shared his views on the newest convention name on this actual matter,

Final 12 months, I referred to 2023 as a brand new age of uncertainty. And that uncertainty prolonged all year long. We skilled continued inflation, rising price of capital, rising geopolitical tensions and shifting perceptions across the Fed’s rate of interest coverage. All of those components contributed to our clients’ rising want for danger administration, capital efficiencies and demand for our merchandise. Following the very robust efficiency of our enterprise in 2022 and 2023, we now have seen the hypothesis that our rate of interest enterprise might face headwinds primarily based on the expectation that the Fed will begin to decrease rates of interest this 12 months. In my 40-plus years within the trade, I’ve noticed that no matter whether or not charges are going up or down, our volumes are sometimes increased in periods when the change of charges is unsure as is the case at this time.

And the very fact is no person is aware of when would charge cuts come. Within the newest twist on this rate of interest lower narrative, Fed Chair Jerome Powell signalled that rate cuts would be delayed – again. In different phrases, the tailwind that benefited CME income and earnings development from 2022 to 2023 may very well be anticipated to proceed.

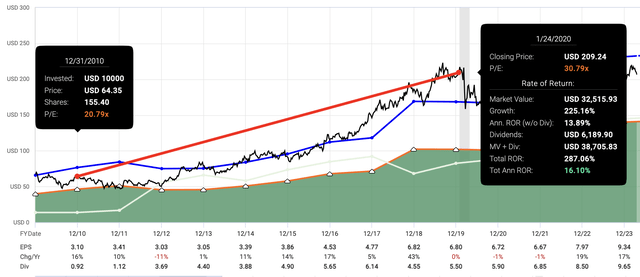

Secondly, over the previous 20 years, CME has been producing optimistic earnings and rising income yearly. Not even throughout the Nice Monetary Disaster nor COVID-19 did CME disappoint with adverse earnings. And keep in mind the world between the Nice Monetary Disaster and the Covid disaster had been a low-interest charge one, the form of analysts are involved about, and CME continued to present shareholders a really first rate 16.1% annualised charge of return.

Fastgraph

Thirdly, I like CME’s enterprise mannequin. The world continues to be a unstable with uncertainties at each nook. Businessmen, merchants, institutional buyers, retail buyers – all of them want instruments to handle these uncertainties. In response to the corporate’s 2023 10K,

CME Group allows purchasers to commerce futures, choices, money and over-the-counter (OTC) merchandise, optimize portfolios, and analyze information – empowering market members worldwide the power to effectively handle danger and seize alternatives…

Our merchandise present a way for hedging, hypothesis and asset allocation associated to the dangers related to, amongst different issues, rate of interest delicate devices, fairness possession, adjustments within the worth of overseas forex and adjustments within the costs of agricultural, power and metallic commodities…

The shopper base of our derivatives exchanges contains skilled merchants, monetary establishments, institutional and particular person buyers, main firms, producers, producers, governments and central banks.

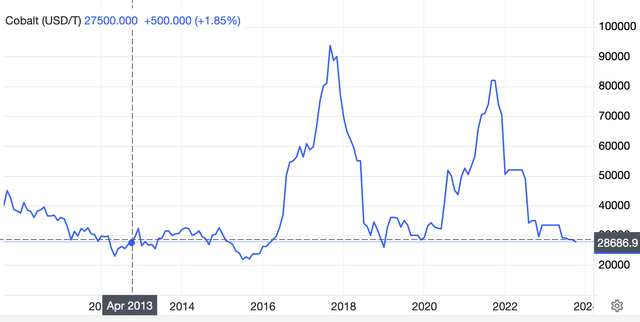

Right here is the place CME is available in. Let’s take electrical car producers for example. Electrical autos manufacturing is determined by metals like lithium, cobalt, nickel, copper, and aluminum. The spot costs of those metals are extraordinarily unstable on the open markets. The chart beneath exhibits the wild swings of cobalt costs over the previous 10 years, from $28686 per tonne in April of 2013 to $95250 per tonne in March of 2018.

Tradingeconomics

CME Group can assist to supply futures and choices contracts on these metals and automakers like Tesla (TSLA) and Normal Motors (GM) can use these to hedge their prices and lock in costs for these metals to make sure extra predictable manufacturing prices. Say Tesla buys a cobalt futures contract that expires in six months at a sure value. This contract obligates Tesla to purchase a hard and fast quantity of cobalt at that predetermined value on the expiry date, so no matter what occurs to the spot value of cobalt within the subsequent six months, Tesla is assured a hard and fast price.

This is only one of quite a few use-cases of how CME’s merchandise can assist its numerous vary of clientele hedge in opposition to dangers. And its buyer base is increasing as CME Group is a worldwide operation. In response to its 2023 10K,

We personal the rights to numerous emblems, service marks, domains and commerce names within the U.S., Europe and different elements of the world. We have now registered lots of our most necessary emblems within the U.S. and different international locations…

Our acquisition of NEX strengthened our function in international monetary markets infrastructure and Information companies, including complementary money and OTC companies and scale to our listed rate of interest and FX merchandise, whereas broadening our international shopper base…

Via the tip of 2023, we now have licensed the CME Time period SOFR benchmark to 2,975 corporations and over 11,000 licensees in 100 international locations.

And with rising dangers and uncertainties being the one fixed, IT is evident that the necessity for CME’s merchandise can be a tailwind for a few years to return.

The opposite facet of CME’s enterprise mannequin is how simply IT scales. Over a interval of 20 years when its internet earnings and income each grew at a CAGR of 17.79% and 12.34% respectively, capital expenditure barely improve at a CAGR 0.97% from $63 million in 2003 to only $76.4 million in 2023. Now, there are unavoidable capital expenditures comparable to upgrades to their Technology platforms to extend capability to deal with bigger buying and selling volumes and to enhance efficiency, and that’s anticipated to rise to $85 million in 2024, these ought to be seen from the lens of the corporate investing in its personal capabilities.

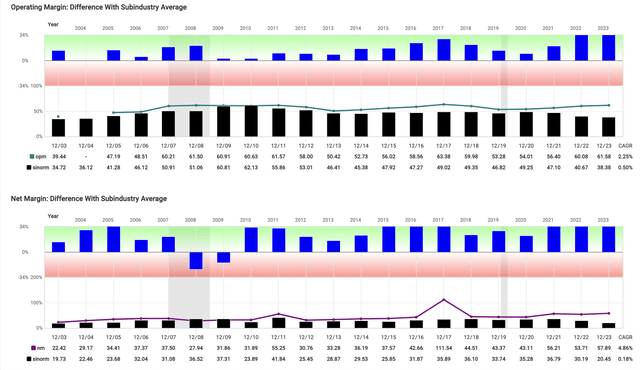

Yet another facet of CME’s enterprise that I like is CME’s can boast that its working margins and internet margins persistently exceed its trade friends.

Fastgraph

If this isn’t a best-in-class enterprise that lets me sleep properly at night time, I have no idea what’s.

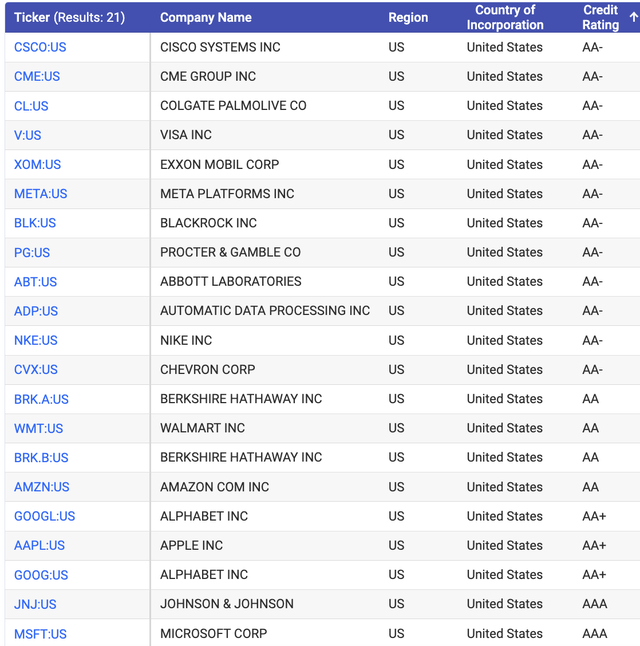

Fourthly, I like CME’s AA- credit standing which in accordance with Commonplace and Poor’s definition of danger CME has solely a 0.55% likelihood of going bankrupt within the subsequent 30 years. Within the unstable and unsure world at this time, only a few firms can boast of getting an AA- credit standing. In truth, solely 21 US integrated firms have credit standing AA- or higher. That offers me peace of thoughts.

Fastgraph

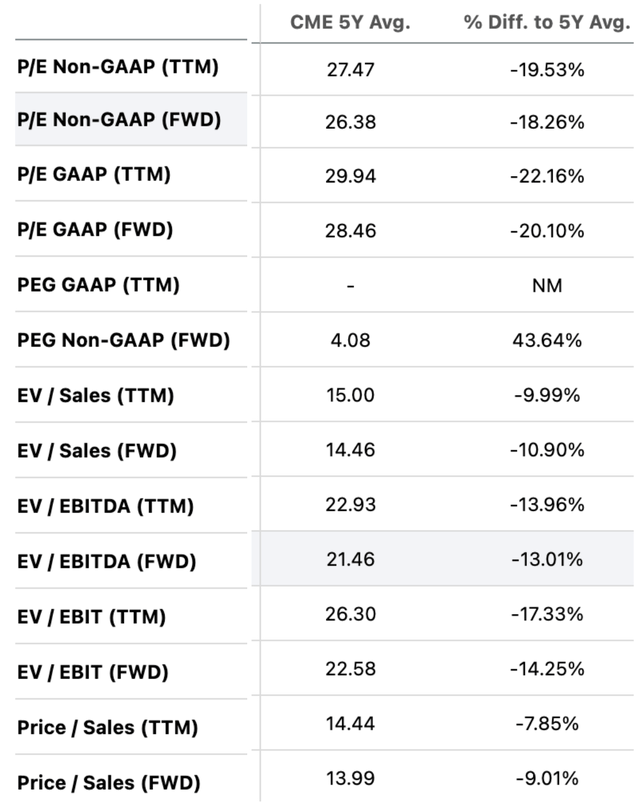

Fifthly, its valuation may very well be compelling right here. Sure, primarily based on my DCF and DDM, CME seems to be overvalued at $210. Nevertheless, primarily based on an absolute valuation foundation, be IT from a P/E or P/S perspective, CME is promoting at a gorgeous valuation in comparison with its previous 5-year common.

Looking for Alpha

Valuation is a perform of value of how a lot buyers are prepared to pay for every greenback of earnings. The intrinsic worth of a inventory could also be a sure determine but when buyers are prepared to pay a premium a number of to personal the shares of that firm, no matter its perceived intrinsic worth?

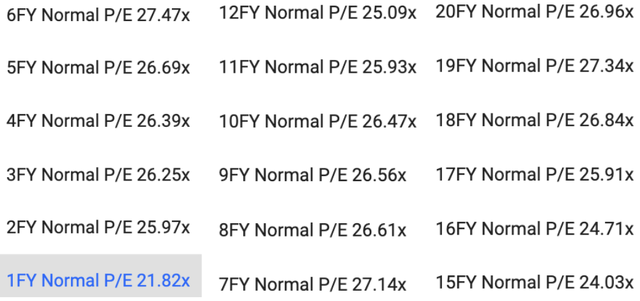

Over the past 20 years, CME has traded at round a mean of 25 to 27 instances earnings. Nevertheless, IT is presently buying and selling at a barely decrease blended P/E of round 22.

Fastgraph

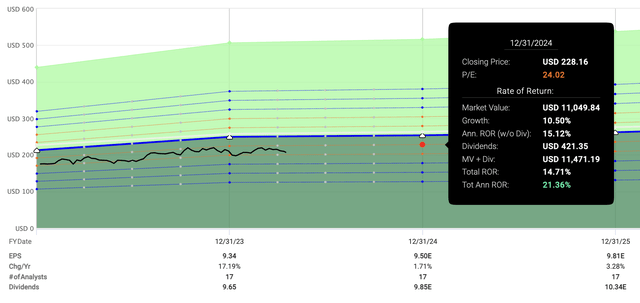

Even a slight blended PE growth from 22 to 24 interprets to a double-digit return.

Fastgraph

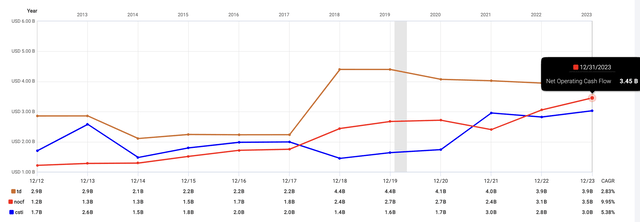

Lastly, CME has been lowering its debt stage aggressively. Sure, CME has some debt however as a clearing home, IT wants liquidity. The maturity of nearly all of these money owed are far off into the long run and the corporate received good charges on them.

CME 2023 10K web page 44

Plus, after I see that an organization’s complete debt ($3.88 billion) could be virtually paid off by lower than 2 years of working earnings ($3.45 billion in 2023), I fear even much less. All that helps me to sleep properly at night time.

Fastgraph

Conclusion

An funding that issues to me in periods of uncertainties is one which lets me sleep properly at night time., and CME Group is one such firm. CME Group is an AA- rated firm that has generated optimistic earnings yearly within the final 20 years, be IT in a low-interest charge surroundings or a high-interest charge one. Its enterprise mannequin caters to a various and international clientele from greater than 100 international locations to satisfy their must hedge in opposition to danger. IT is a particularly scalable enterprise that requires little or no capital expenditure to take action. And CME have to be doing one thing proper to persistently surpass its friends in internet earnings margin and working earnings margins.

No, CME just isn’t strictly a value-buy proper now and pure worth buyers can select to attend for the costs to fall additional. Nevertheless, I’ve chosen to begin a 25% place on the present value of $206 in what I consider to be a large moat firm, getting ready so as to add extra if IT falls to what I consider is its honest worth.