nikom1234/iStock through Getty Photographs

The telecommunication corporations within the communication sector usually stand out for top yield, with the 4 reviewed on this article being in that class. In addition they have investible S&P credit score rankings together with 6%+ dividend yields. To notice is that one in all them goes to chop the dividend in 2025 and will nonetheless have a 6.1% yield. IT is vital to notice that telecom service suppliers will not be in favor, however what makes them well-liked to personal is that they do present fairly dependable high-yield earnings.

Present costs with Morningstar and Worth Line Worth Targets

To introduce the tickers and names, I’ll begin with some present costs after which pricing analyst estimates from Worth Line and Morningstar. They need to be used as factors of reference as extra Information is revealed for every particular person inventory. BCE Inc. (NYSE:BCE) would be the focus of this text, however the others that additionally provide a bit decrease excessive yield will get a shorter evaluation. The “Rose Take and Suggestion” is supplied for every one and will provide you with an thought of their future throughout the “RIG” portfolio.

Abbreviations used within the chart:

Present $Pr/Sh = US$ Worth/Share on June 15, 2024.

M* = Morningstar Analyst premium subscriber Information

M* FV = Truthful Worth from Morningstar analyst premium Information.

M* Purchase = the low purchase worth goal instructed.

VL = Worth Line analyst security score, with a 1 being the perfect, 3 common and 5 the worst.

MidPt Worth = Worth Line Worth Goal in US$ for the tip of 2025.

|

S&P |

Inventory |

Firm |

Present |

M* |

M* |

VL |

MidPt |

|

CR |

Ticker |

Identify |

$Pr/Sh |

FV |

Purchase |

Worth |

|

|

BBB+ |

(BCE) |

BCE, Inc. |

32.88 |

44.00 |

35.20 |

2 |

36 |

|

BBB |

(T) |

AT&T |

17.64 |

23.00 |

16.10 |

2 |

16 |

|

BBB+ |

(VZ) |

Verizon |

39.67 |

54.00 |

37.80 |

2 |

36 |

|

BBB |

(VOD) |

Vodafone Group |

8.74 |

15.00 |

10.50 |

3 |

8 |

BCE

BCE Inc.- 8.9% yield

BCE is the first focus of this text getting extra intensive protection for its 8.9% dividend yield and that IT is my most up-to-date buy, proudly owning IT together with all the remainder. I had bought my shares final 12 months after I wrote an article in Could 2023 suggesting earnings had been in decline and the dividend probably wouldn’t rise a lot, if in any respect. The worth most positively sunk, whereas administration allowed the dividend to remain intact and even raised IT as promised. With that dividend promise in thoughts and earnings seeking to stabilize, IT is sitting fairly with that 8.9% yield and probably a worth under truthful worth. Statistics for P/E and earnings had been obtained from Quick Graphs, a subscriber service I take advantage of.

IT was based in 1880 and is headquartered in Verdun, Canada, and IT controls about 75% of the fastened line telecommunications community there.

On the finish of 2023 IT was at over 80% full, bringing fiber connections to over 7 million houses and provides a aggressive benefit for 5G that might drive future outperformance.

IT is tied with the mixed Canadian corporations of Rogers/Shaw with presently having ~4.5 million web clients.

IT additionally has a top-grade prime quality diversified media unit “Crave”, which provides video on demand together with HBO, Showtime and Starz together with proudly owning CTV and TSN “Prime Sports activities”.

Earnings/Money Move

IT reported a lower in income by 16% in Q1 2024 from Q1 2023 together with flat adjusted EBITDA. Elevated depreciation and amortization bills together with elevated curiosity prices resulted within the lackluster revenue and sadly, would possibly simply keep that means this 12 months.

Extra on the optimistic aspect, revenues noticed a slight enchancment within the CTS section or communications Technology providers for brand new cellphones, elevated web subscribers and likewise seeing elevated working efficiencies that offset declines in legacy voice knowledge satellite tv for pc TV providers.

The workforce discount and restructuring from 2023 ought to begin to present extra optimistic money flows later this 12 months.

Analyst “Worth Line” signifies full-year EBITDA ought to enhance, however solely by low single digits.

Headwinds/Detrimental Facets

-Canadian elevated regulatory rulings, particularly for broadband.

-Addition of a 4th wi-fi competitor reminiscent of Quebecor

-An excessive amount of publicity to landline and video providers

-Decreased satellite tv for pc subscriptions

-Not proudly owning its personal media content material and rising licensing prices for IT.

Tailwinds/Constructive Facets

-Subscriber development as a consequence of rising immigration from different international locations

-Pension plans had been totally funded on the finish of 2023.

-The prices for Quebecor to create new traces and compete could be overwhelmingly costly and probably would imply they would wish to accumulate Freedom Cell and its present traces.

-Present buyer reliance on wi-fi and broadband ought to proceed and enhance.

All in all, income development is proscribed secondary to the aggressive nature and will advance at low single digits or solely ~2% yearly.

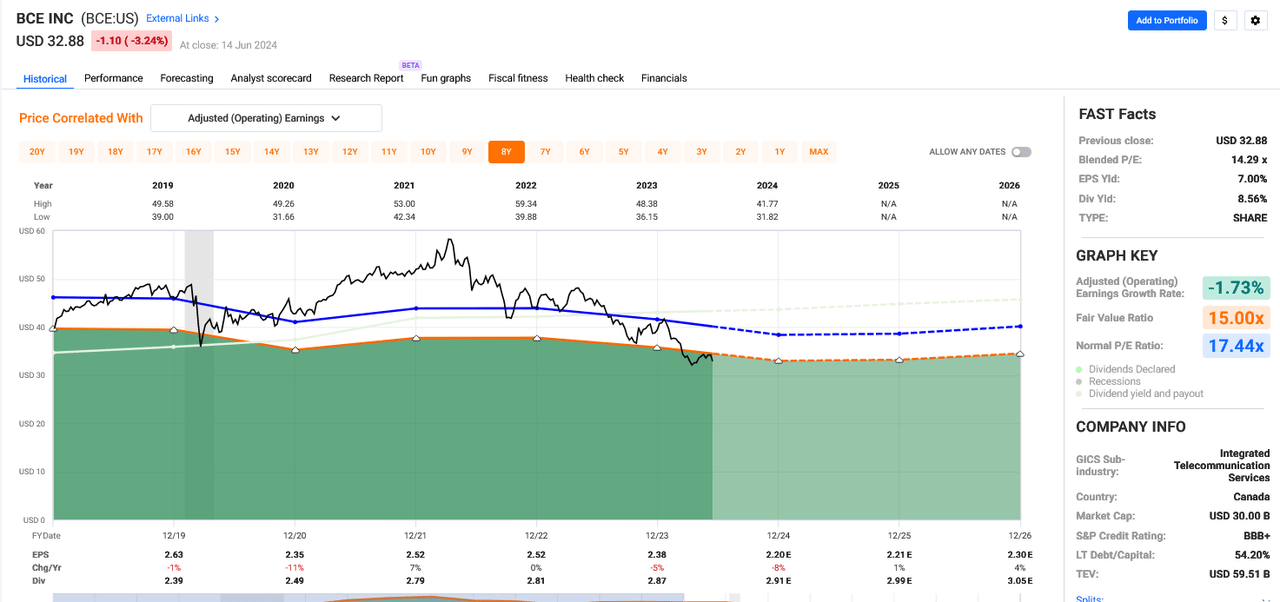

FAST Graphs – “FG”

The next colours/traces on the “FG” chart proven under signify:

Black line = worth.

White line = dividend.

Orange line = Graham common of often 15 P/E “worth/earnings” for many shares.

Blue line = Regular P/E.

Dashed or dotted traces are estimates solely.

Inexperienced Space represents earnings.

Statistics by 12 months are famous for top and low costs on the high of the chart in black, and for earnings and dividends on the backside of IT. The % proven is for the change from 12 months to 12 months for earnings, with an E after any quantity representing an estimate. The 8-year FG under is for six previous years and a pair of future estimates.

BCE Technical 8-year chart (FAST Graphs June 15, 2024)

The worth has now sunk underneath the truthful worth orange line of 15 P/E. IT presently sells at 14.29x, which is under the 17.44x regular blue line. That might make IT undervalued by that metric.

The worth decline probably resulted from its poor earnings/decline during the last 12 months and now into 2024. Earnings estimates look to stabilize and virtually flat line by way of the remainder of 2024 after which begin rising ever so barely in 2025.

Dividend

2018, 2019 and 2020 noticed earnings declines, however the dividend was maintained and even raised, revealing administration’s dedication to sustaining and even elevating IT. Excellent news for shareholders, however nonetheless considerably unnerving when wanting on the earnings chart and the dividend line in IT.

The dividend white line can barely be seen within the FG above, as IT doesn’t seem within the inexperienced space of earnings. IT is using excessive above within the white space, which implies IT is just not totally funded from earnings and has an precise payout per FG of 120.5% which has now been over 100% since 2020.

The excellent news is that long-term debt /capital is 54.2%, and IT can proceed funding the dividend if IT so chooses. The leverage ratio is low and consistent with its friends. IT has been instructed inventory repurchases is likely to be a greater use for its money, however so far administration has indicated IT is resolved to proceed the dividend at its present degree, which, once more, is superb information for shareholders.

The 2023 dividend was $2.87 US and is estimated to be $2.91 for 2024, a 1.4% elevate.

The 5-year DGR is 4.5%, however as talked about above the raises are on a decrease % elevating pattern, however 2024 is estimated by FG to rise by 2.7% to $2.99. I consider that to be beneficiant, however probably doable if one seems at money flows.

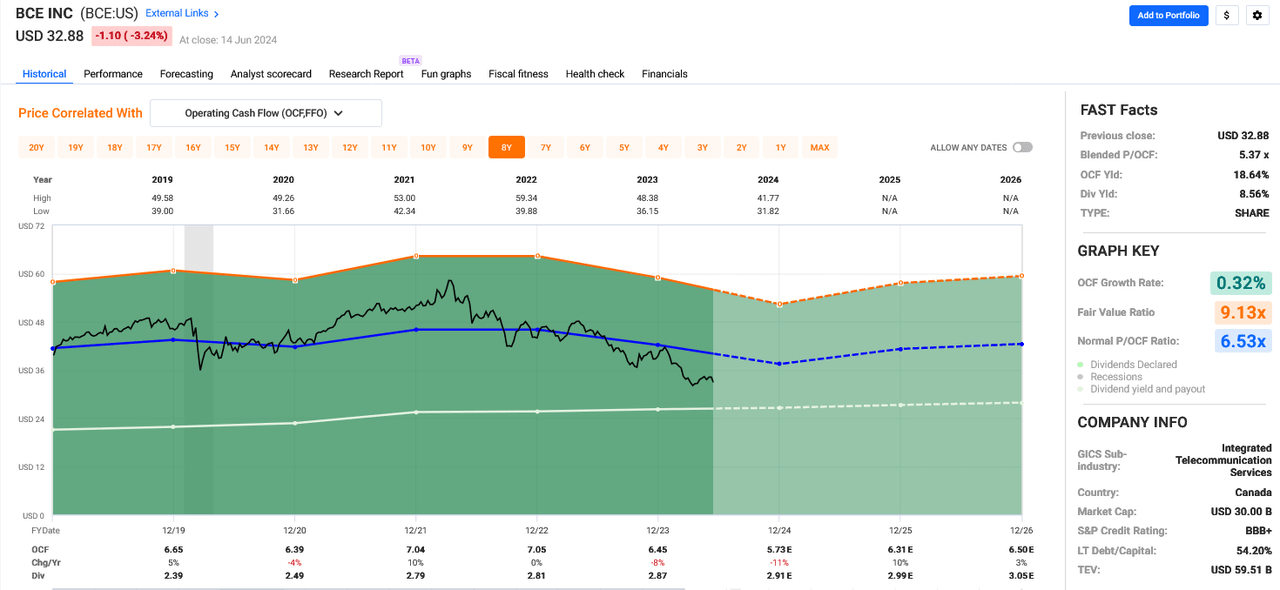

Money Flows FG

BCE Money Move 8-year technical chart (FAST Graphs June 15, 2024)

The FG above reveals the dividend is roofed and the P/OCF or Worth/Working Money Flows is 5.37x, the place the conventional or blue line is 6.53x. Positively excellent news for the dividend.

Chowder #

C# = 5-year dividend development fee + yield = 13.4, however bear in mind telecoms solely want an 8, so BCE passes on its yield alone, which is presently a tremendous 8.9%.

Rose Take and Suggestion

The dedication by administration to maintain the dividend and even elevate IT together with the value falling under 15x P/E satisfied me to start out a place in March when IT had an 8.5% yield. The M* Purchase worth above within the chart of $35.20, and IT positively is now under that. The now 8.9% is a superb yield for anybody needing earnings from a high quality Canadian firm, and I say IT is a Purchase. With telecoms being out of favor, capital features won’t be seen for years. Observe the international tax is deferred in an IRA of any sort and could be recovered in a taxable account at tax time.

ATT Inc. – 6.3% yield

T offers telecommunication and Technology providers worldwide, together with a Latin America section that operates in Mexico. The corporate previously often known as SBC communications modified its title in 2005 to AT&T Inc, was integrated in 1983 and relies in Dallas, TX. IT has a $126.48B market cap.

IT cut up off its owned portion of Warner Media (WBD) in April 2022 giving shareholders 0.024 shares for every T share owned and reduce the T dividend to 27.75c/ quarter the place IT has been ever since.

Earnings look to be flat for now after falling the final 2-3 years. They sit at $2.22 per share for 2024 and are estimated to rise 3% to $2.30 in 2025 and up 6% to $2.44 in 2026.

IT has a BBB S&P credit standing and has a stagnant dividend presently at $1.11 yearly, giving IT on the $17.64 worth a yield of 6.3%.

No dividend development because the cut up in 2022.

The payout is 46%, so there could possibly be room to boost the dividend.

Lengthy-term debt/capital is 56.17%.

Money move P/OCF for 4 years is 4.12x, and IT is presently at 3.36x, all good.

Chowder# is 6.3 based mostly on its yield alone. With any kind of dividend elevate, IT might rise to get to the passing grade of 8.

The present P/E is 7.59x and regular 5 years is 7.89x; subsequently IT sits very a lot at a stagnant degree for worth as effectively.

Rose Take and Suggestion

I personal IT, have held IT a very long time, do not love IT, however the earnings is okay. There are lots of higher selections for earnings with larger yields, however these may also bear extra danger. IT offers dependable earnings at a greater yield than most CDs. IT is a purchase if the value dips once more, however for now, I hold IT in RIG, IT is a Maintain.

Verizon – 6.7% yield

VZ engages within the offering communications, Technology, Information, and leisure merchandise for customers and companies worldwide. IT was previously often known as Bell Atlantic Company “SBC” and adjusted its title to Verizon Communications in June 2000. IT was integrated in 1983, is headquartered in NY, NY. and has a BBB+ S&P credit standing. IT has a $166.98B market cap.

Earnings began to fall in 2022 by 4% after being up 10% by way of 2021 at $5.31. Nonetheless, earnings fell by way of 2023 by 9% and a smaller quantity going into 2024, sitting now at a low of $4.60. 2025 & 2026 estimates look to rise by 3% annually, with $4.88 for 2026.

The P/E regular for six years is 10.39x, however has now shrunk to 9.31x for 4 years. IT is presently promoting at 8.51x. IT is undervalued by that metric.

Lengthy-term debt/capital is 57.69%.

Dividend payout is 55.68% which could be very common and simply advantageous.

Regular P/OCF is 4.99x, and IT is now at 4.53x, which makes IT all good for overlaying bills and the dividend.

The 5-year DGR is 2% and the ten 12 months can also be fairly comparable at 2.37%. IT has paid rising dividends for 19 years.

C# = 8.7 and passes that check for buy.

Rose Take and Suggestion

I sincerely have all the time preferred this firm and getting these 2% dependable raises. IT‘s staying, and if its worth ought to dip once more underneath $35, I like to recommend anybody with out IT contemplate proudly owning IT for earnings. $33.63 = 8% yield. That might be arduous to disregard, even for me.

Vodafone Group – 11.1% yield

VOD provides providers within the UK, Europe, Turkey, Germany and Africa. IT most not too long ago bought its operations in Italy for $4.5B and $1B in Desire Shares and Spain for $8.8B, whereas decreasing its Indian three way partnership by $2.4B. These divestitures will assist transfer IT to extra share buybacks estimated to be $4.4B per the analyst “Worth Line”.

IT is agreed to mix the UK enterprise with Three UK to create a 3rd scaled community operator there. IT has plans to merge with CK Hutchison and can personal 51% of that superior standalone 5G community.

Development ought to rise, however from a smaller base and is difficult to check with previous outcomes. Nonetheless, natural service revenues did develop by 6.3% in 2023.

Overseas corporations like this one pay dividends solely 2x per 12 months.

Vodafone has an ex date in November to announce the dividend to be paid in February, which was 48.15c in 2024. IT simply had an ex-date on June seventh to announce the 48.601c IT can pay August 2nd. This quantities to 96.75c for the 2024 12 months and offers IT a yield of 11.1% at its present low worth of $8.75.

Dividend Reduce Coming

IT is thought and administration has introduced that the dividend will probably be reduce by ~50% for 2025. Estimates point out IT probably will probably be ~27c for every 2x yearly fee and takes the dividend yield all the way down to ~6.1% if the value stays at $8.75. This yield is consistent with most different telecoms.

Regular 4-year P/E is 11.39x, and IT is 10.27x presently however would drop secondary to the latest divestitures. Earnings are estimated to rise again up slowly to the 2023 degree of $1.22 someday in 2027.

Lengthy-term debt to capital is 41.32%.

4 years P/OCF is 2.09x and stands at 1.54x immediately and may do effectively with the dividend reduce.

Complete return prospects, even with the dividend reduce, look to supply good return over a 3-5 12 months span.

C# = 11.1 which passes alone with its present yield, however not into the longer term with the anticipated dividend reduce.

Rose Take and Suggestion

IT is attention-grabbing to notice that M* has the purchase worth at $10.50, which is larger than the $8.75 now, which is encouraging and reveals potential. IT is an actual conundrum, providing good earnings even with a future dividend reduce. At the least administration is sincere and foretold the occasion and is streamlining this very complicated, overgrown firm. I admit to being upset for some years with the value and would contemplate streamlining my holdings if IT ought to rise larger, which is uncertain. The worth now’s low and if IT goes decrease to $6.75 or 8% yield, IT could be a screaming purchase. I’ll proceed to maintain with full data of a dividend reduce in 2025.

Abstract/Conclusion

Protection in an earnings portfolio additionally means shopping for at nice worth, high quality corporations with dependable dividends that present good earnings. All 4 of those telecom corporations have good S&P credit score rankings and supply some earnings protection with their excessive yields. Capital features is not going to be forthcoming rapidly with any of those corporations. Raises are all the time welcome, and so persistence for the appropriate purchase worth is typically the toughest to overcome for many traders to herald a better complete return. The “RIG”/ Rose’s Earnings Backyard portfolio was constructed with persistence and nice worth. Worth is up 6.61% YTD and beating SPY by 3.33% since inception November 2021. IT additionally has a dividend yield of 6.2% and subsequently dividends for earnings stays a powerful driver for the 85-stock portfolio. These 4 telecom shares will stay for now within the “RIG” portfolio, as they meet most necessities for membership.

👇Observe extra 👇

👉 bdphone.com

👉 ultraactivation.com

👉 trainingreferral.com

👉 shaplafood.com

👉 bangladeshi.help

👉 www.forexdhaka.com

👉 uncommunication.com

👉 ultra-sim.com

👉 forexdhaka.com

👉 ultrafxfund.com

👉 ultractivation.com

👉 bdphoneonline.com