Larry Humphreys, a retired Federal Emergency Administration Company employee in Moultrie, Georgia, says he and his spouse received’t be touring a lot subsequent yr after their month-to-month Health insurance coverage premium fee will increase greater than 40%, to $938.

Humphreys, 68, feels betrayed by the Federal Workers Health Advantages Program. “As federal workers, we sacrificed good salaries within the personal sector as a result of we thought the advantages from authorities could be higher now, in retirement,” he mentioned.

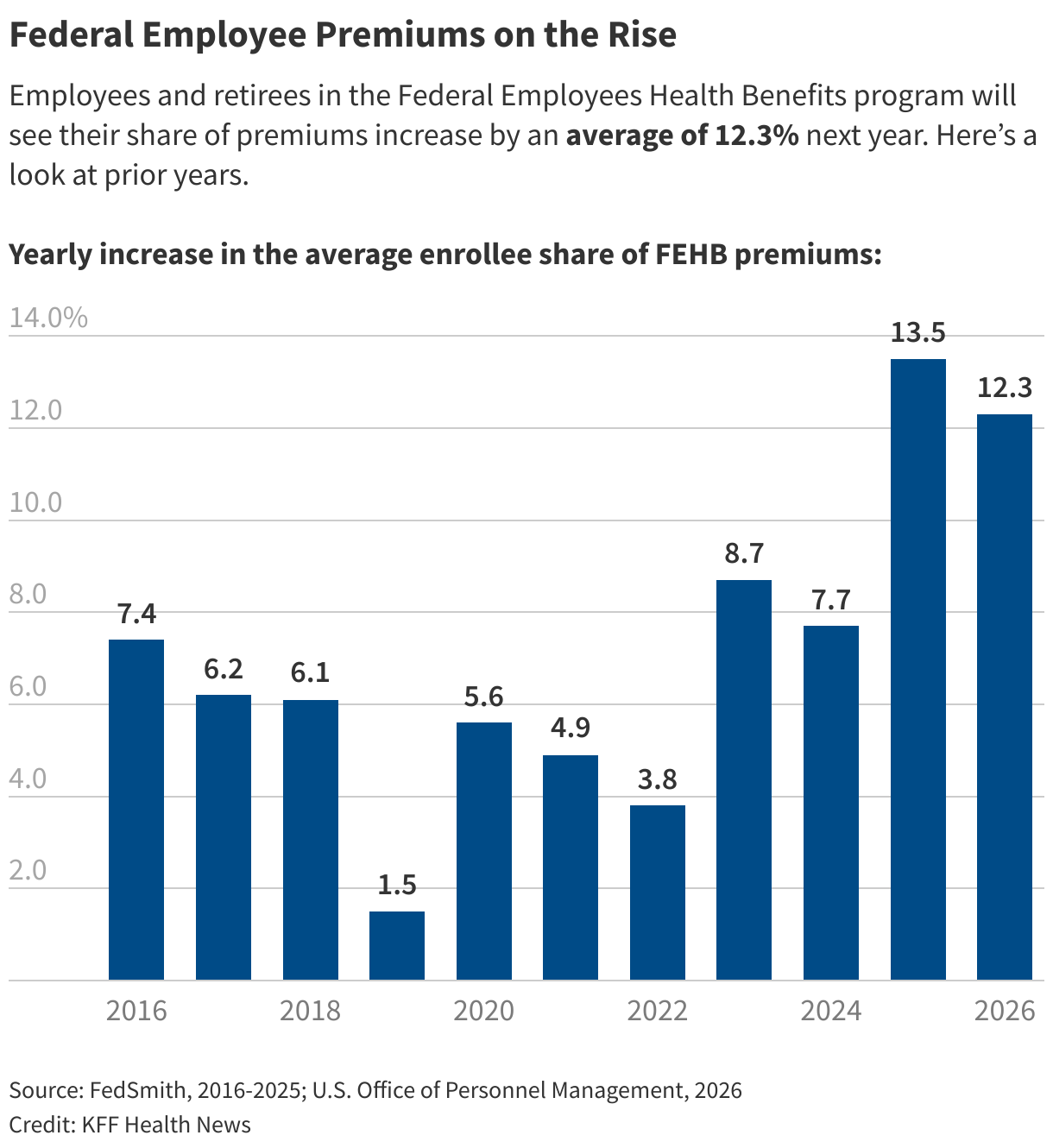

Because the nation’s largest employer-sponsored Health insurance coverage program, the FEHB Program covers greater than 8.2 million federal authorities workers and retirees, and IT was as soon as celebrated as a nationwide mannequin for controlling prices whereas giving enrollees many Health plan choices.

However subsequent yr, common enrollee premium funds within the system are set to leap greater than 12%, on high of a 13.5% hike in 2025. The 2-year enhance is greater than what many personal employers and their employees are experiencing.

The FEHB charge hikes are just like these for plans offered on the Inexpensive Care Act exchanges — excluding the federal government subsidies most enrollees get, a serious level of competition on Capitol Hill. The premiums insurers cost for Obamacare plans are rising 26% on common for 2026, following a 4% enhance this yr.

What’s making the most recent hike in FEHB premium funds even tougher to abdomen for tens of millions of federal workers is its timing: The 2026 enhance was introduced in October, when many federal employees have been on unpaid furlough through the 43-day authorities shutdown.

Not like most personal employers, the FEHB Program offers its enrollees quite a few Health plans to select from. That permits some folks to decrease their month-to-month premium funds by switching to plans with greater deductibles or copayments. However every year only about 5% of enrollees swap plans, in response to the Workplace of Personnel Administration, which oversees this system.

Humphreys, who has stayed with the identical Health plan for many years regardless of steadily greater costs, mentioned IT’s troublesome figuring out which plan is greatest primarily based on their Health circumstances. He has glaucoma and diabetes, and his spouse, Julianne, has confronted coronary heart points.

Their FEHB plan covers prices for his or her care not lined by Medicare, which usually pays 80% of their Health payments.

“There’s a concern that if you happen to do one thing and alter plans and IT’s flawed, you could possibly be in a foul spot,” he mentioned.

Open enrollment for federal workers and retirees runs by way of Dec. 8.

Among the many components inflicting premiums to extend, in response to OPM, are an getting older federal workforce with extra power circumstances, in addition to prescription drug use, together with expensive GLP-1 drugs for weight reduction.

About 42% of federal workers are over the age of fifty, in contrast with 33% within the normal workforce, OPM says. About 7% of federal workers are beneath the age of 30, in contrast with about 20% of employees total.

OPM officers mentioned the Trump administration’s insurance policies geared toward reducing drug prices and centered on prevention of pricey medical circumstances will hopefully assist IT management premiums sooner or later.

“None of those initiatives after all will occur in a single day – turning a $79 billion ship takes gradual and regular progress,” Shane Stevens, OPM’s affiliate director for Health Care and insurance coverage, said in a news release. “However, we’re dedicated to bettering the standard of life and high quality of look after our members whereas additionally guaranteeing that healthcare stays accessible and inexpensive for many who work (or have labored) for the American folks.”

OPM didn’t reply to requests for remark.

John Holahan, a Health coverage fellow on the nonpartisan City Institute, mentioned OPM’s rationalization disregarded a key cause for rising premiums: hospital consolidation. Whereas the FEHB Program is a group of Health plans, in lots of markets — together with the Washington, D.C., space — these insurers should negotiate with a handful of highly effective Health methods which have purchased up different hospitals and medical doctors. That market energy allows them to drive costs greater on FEHB plans, he mentioned.

Jacqueline D. Bowens, president and CEO of the D.C. Hospital Affiliation, mentioned in an announcement that “the prices borne by sufferers usually are not decided solely by the care they obtain, however by how insurance coverage corporations select to cost, reimburse, and prohibit entry to that care.”

Holahan mentioned IT’s shocking that FEHB premiums are rising even quicker than these of different, smaller employers. However he’s not shocked federal workers don’t swap plans extra typically, even when IT could also be of their monetary curiosity.

“IT’s that individuals discover the Health Care world so difficult,” he mentioned. Holahan, a famous Health economist, mentioned he, too, finds IT daunting to modify Medicare Health plans.

Mike Lindquist, a scientific assessment officer for the Nationwide Institutes of Health, mentioned he’s not pleased with the rise in his premium funds the previous two years. “IT’s robust, as IT’s a giant expense.”

Lindquist, 43, who lives in Brunswick, Maryland, has been on the identical Blue Cross and Blue Protect plan by way of the FEHB Program the previous few years although he evaluates his choices every fall.

“By not switching, you don’t have to fret about selecting a brand new plan that may not take your practitioners,” he mentioned.

Jonathan Foley, a Health guide who labored as a senior adviser at OPM through the Biden administration, mentioned premium will increase will probably be a hardship for a lot of enrollees. Whereas the FEHB Program gives 200 Health plans in complete, with about 10 to twenty in every geographic market, enrollment is concentrated in only a handful of Blue Cross and Blue Protect plans.

“This focus reduces competitors and offers outsize affect” to charge will increase by Blue Cross and Blue Protect, Foley mentioned in an e mail.

He mentioned the FEHB Program additionally faces greater prices as a result of IT requires its Health plans to cowl GLP-1 drugs, corresponding to Wegovy and Ozempic. Nationally, fewer than half of huge employers supply this profit, in response to the Peterson Center on Healthcare and KFF. KFF is a Health Information nonprofit that features KFF Health Information.

One other value strain has been extra members utilizing behavioral Health advantages to deal with despair and anxiousness for the reason that begin of the covid pandemic, Foley mentioned.

The Trump administration’s federal workforce reductions even have contributed to value will increase, Foley mentioned. OPM has misplaced a couple of third of its workers previously yr, leaving fewer employees to supervise the FEHB Program and negotiate with dozens of Health insurers, he mentioned.

“The workforce reductions and the unpredictable nature of policymaking within the Trump administration has created appreciable uncertainty amongst Health insurance coverage carriers,” Foley mentioned. “The response of actuaries to elevated uncertainty is to lift charges.”

A Government Accountability Office report this yr discovered that current OPM staffing vacancies led to a suspension of fraud threat assessments within the FEHB Program.

John Hatton, employees vice chairman for coverage and packages at an advocacy group referred to as the Nationwide Energetic and Retired Federal Workers Affiliation, mentioned greater costs imply IT’s important for FEHB members to buy and examine plans for subsequent yr. “This system was designed to advertise competitors to mitigate and drive down prices,” he mentioned.

Hatton mentioned OPM surveys present the primary causes folks don’t change plans is they’re overwhelmed by their choices and nervous about making a mistake. Switching to a plan with even a barely greater deductible, he mentioned, might save folks a number of hundred {dollars} a month on premiums.

However Humphreys, the Georgia retiree, mentioned he likes that his present plan comes with low out-of-pocket prices for him and his spouse. They owed little cash when his spouse suffered a kidney stone an infection and sepsis, which put her within the hospital for 12 days.

That reassurance will quickly come at a better value: Their FEHB and Medicare premiums will take up greater than half of his pension examine subsequent yr after accounting for taxes.

“I can take a lower-premium plan, however IT’s a chance I’m not prepared to take,” he mentioned.

👇Observe extra 👇

👉 bdphone.com

👉 ultractivation.com

👉 trainingreferral.com

👉 shaplafood.com

👉 bangladeshi.help

👉 www.forexdhaka.com

👉 uncommunication.com

👉 ultra-sim.com

👉 forexdhaka.com

👉 ultrafxfund.com

👉 bdphoneonline.com

👉 dailyadvice.us